Vmoto (ASX:VMT): Riding the EV Megatrend on Two-Wheels

Vmoto manufactures and distributes electric-powered two-wheel vehicles combining low-cost Chinese manufacturing capabilities with European inspired design.

In my last deep-dive on LaserBond, I mentioned how I believe it is important in this environment to “stay grounded, avoid hot stocks in hot industries, and look for companies that solve a genuine problem, are profitable, growing (primarily through organic growth), founder or owner-operated and are trading at reasonable prices.”

Well, Vmoto is an ASX listed ~107m market-cap company (Using the close price of $0.39 on 22/03/22) that goes against this in some ways, but it is certainly interesting, both from a valuation perspective and the fact that it is still largely undiscovered with significant secular tailwinds at its back. It is a more capital-intensive business than I would generally like to invest in. However, both top and bottom-line growth have begun to show promising signs of future margin expansion and has warranted a small allocation. The company exhibits a lot of the criteria I look for in an investable company, but it also scores half-marks in areas that make me feel less comfortable with making this a larger position, at least until I see some execution in key areas.

This deep-dive will explore what I view to be “full-marks” and “half-marks”.

What does Vmoto do?

Vmoto manufactures and distributes electric-powered two-wheel vehicles combining low-cost Chinese manufacturing capabilities with European inspired design. The company looks to ride the EV megatrend, but with the intention to do so on two wheels, not four.

Many people would not have heard of Vmoto, probably because its wholly-owned 30,000 sqm manufacturing facility is situated in Nanjing, China. However, whilst Vmoto manufactures in China, its corporate office is actually much closer to home in Perth, Western Australia. This came about over a decade ago after Patrick Davin, the founder of Vmoto Limited, brought in Charles Chen, who soon convinced Patrick to set up shop in his hometown of Nanjing. Charles believed cheap manufacturing costs coupled with European inspired design would drive significant future growth, and perhaps up until a few years ago, many would’ve lost faith in Charles’ vision.

Whilst Patrick Davin is no longer at Vmoto limited, Charles Chen is starting to see his vision come to fruition. The company first started producing 2-wheeled vehicles in 2009 and has since grown to build an impressive global distribution network, being represented by more than 53 distributors in approximately 60 countries in the geographic regions of APAC, Europe, South America, North America and South Africa.

Vmoto’s Business Model

Vmoto’s business model includes both Business to Business (B2B) and Business to Consumer (B2C) sales.

B2B is where Vmoto supplies its products to companies, including food delivery, parcel delivery and ride-sharing companies. B2C is where Vmoto’s electric mopeds/motorcycles are sold directly to consumers throughout the world.

Business 2 Business

The Vmoto E-Max range of electric mopeds are targeted at food delivery, parcel delivery and ride-sharing companies. They’re highly customisable to carry heavier loads and travel longer distances.

Ride-Sharing

As of November 2021, Vmoto had eight ride-sharing customers, a one customer increase on FY20.

In January 2021, following the delivery of 4,300 units in FY2020 to Go Sharing (a subsidiary of Greenmo Group), Greenmo Group ordered a further 5,904 units worth an estimated $13 million. This repeat order was the largest to date and highlighted the significant opportunity at play here.

The beauty of this is that as these ride-sharing companies grow, so too should the volume and magnitude of repeat orders, or so I hope as part of my thesis. Greenmo Group is pursuing an aggressive expansion plan with early signs of expansion into Turkey, Austria, Belgium and Germany. Provided the relationship remains strong with Greenmo Group, you’d expect to see future orders to roll out this expansion. The margins from this side of the business can range between 25–35%, due to high volume sales. This is also an area that might see margin expansion over time as bulk orders can provide an opportunity to improve operational efficiencies compared to smaller & more bespoke orders.

Delivery

Vmoto’s delivery partners grew to 12 delivery customers by FY2020 and has since added three new delivery customers as of November 2021. This is perhaps an area I am most excited about. Vmoto only needs to sign a few big deals here to fuel future growth. Food delivery is a huge growth area and an area that doesn’t require cars. Companies that want to reduce their carbon footprint (which I believe many will over time) will phase out petrol & diesel mopeds/motorcycles and look for alternatives. In FY2020, Vmoto stated they were in discussions with an additional 13 delivery customers, with the potential to be their supplier of choice.

Last year Vmoto partnered with Helbiz (NASDAQ: HLBZ) to deploy Vmoto Soco electric mopeds to run the Helbiz Kitchen operations in Milan. More recently, Helbiz and Vmoto have expanded this partnership with an agreement to supply an additional 2,000 electric mopeds to Helbiz for deployment throughout Italian cities.

A quick look at Helbiz, and it seems like a very early-stage company with LTM revenue of ~US$10m (according to Tikr), so the growth here is worth keeping an eye on as it could determine how large or small future orders may be. If successful, it wouldn’t surprise me to see Helbiz order more Vmoto mopeds for deployment potentially in the US market, where Helbiz’s headquarters are located.

In March 2021, Vmoto announced an MOU signed with Bird Group of India. India represents a massive opportunity for Vmoto if this story plays out. India is the largest internal combustion engine (ICE) two-wheeler market in the world, and the Indian two-wheel EV market size is expected to reach USD750 million by 2025.

If Bird Group’s technical evaluations of Vmoto Soco’s two models, the CUX and CUmini are successful, then Bird Group will order a minimum of 10,000 units in the first year, equivalent to approximately AUD $13.8m. This would mark the largest order to date, exceeding the order from Greenmo Group. Since then, I have not been able to find updates on the progress here, but I’ll certainly be watching for them. Success here could represent an enormous opportunity.

One consideration of the Indian landscape is India’s ban on imported finished goods. The Indian government is focused on localisation, so the way Vmoto does business in future with India could be much different to the type of business we see today in other countries. I.e. Instead of exporting the finished mopeds/motorcycles into India, it might require Vmoto to export the parts to a strategic manufacturing partner in India who has the know-how to assemble the bikes. Personally, I’m not sure how the margins would differ on this ‘style’ of business and it is something I hope to gain clarity on in future.

Europe undoubtedly dominates Vmoto’s B2B operations, so progress in markets such as USA, India and Australia should be monitored.

Business 2 Consumer

Within B2C, there are a few brands. Firstly, Super Soco is a third party brand that Vmoto holds exclusive marketing and distribution rights into international B2C markets (excluding China). These products are manufactured under a 50/50 joint manufacturing agreement at Vmoto’s facility in Nanjing to capitalise on better production efficiencies and cost synergies. The motorcycles/mopeds are targeted to appear fun and trendy.

You be the judge of that below…

I think the Vmoto Soco brand looks both classy and trendy, but appearance is only part of the selling point. When it comes to winning new customers, I believe potential customers that aren’t “full greenies” will need to see performance that can reasonably compete with that of 2-wheel ICE vehicles. This comes down to three components; Speed, Range & Charge-time.

Taking a look at speed, Vmoto Soco’s products start at a max speed of 45km/h and go up to ~95–100km/h (excluding the new premium range, which I’ll discuss later). The bikes tend to have a range of 75km all the way up to 200km with a dual battery. However, it’s important to note that these features are on the assumption of travelling 45km/h with a 75kg person.

Higher speeds and longer ranges aren’t necessarily required for European countries and areas where inner cities are geographically dense. However, to win customers where higher speed limits and longer commutes typically exist, we’re going to need to see future models that showcase this. Charge times will also need to improve as currently charge times range between 3.5 hours to 7 hours. Comparing older models to newer ones shows this improvement, but there is still a long way to go. So on that note, I have to give the performance “half-marks” for now, but there is potential for “full-marks” in future. I just hope this is before new entrants or existing incumbents capitalise on the two-wheel EV megatrend.

Importantly, Vmoto’s sales into China are a very small portion of overall sales. According to the 4Q21 update, “Vmoto sold a total of 7,410 units, with more than 93% of units being sold into international markets, while just under 7% of units were sold into the Chinese market”. This is encouraging to see because it shows Vmoto’s strategy focused on the higher-margin, less competitive landscapes (for now) in international markets.

Looking forward, the channel through which Vmoto chooses to sell into new markets is important. Navigating the landscapes could be challenging as each new market and jurisdiction can differ from one another. As a result, the choice of the channel has the potential to determine the level of success or failure of global expansion.

Do they choose to sell through a distribution agreement or to a strategic partner? Decisions like these determine the level of involvement from Vmoto. For example, they could choose to sell to a distributor without any further involvement, or do they take part ownership in the distribution business by investing in it and then personally try to drive greater orders. These decisions are hard to forecast, but I imagine management will continue to pursue a mixed basket approach.

Vmoto’s Business Structure

The business structure is fundamental to understand as it’s changed over the past couple of years, and I’m still trying to wrap my head around it.

Below is a screenshot from the July 2020 Investor Presentation. Here you can see Vmoto is made up of a few components.

In early 2020, Vmoto established a new jointly owned (50/50 split) manufacturing company with Super Soco to become “Vmoto Soco”. Subsequent to this, Super Soco is to transfer all of its production and supply chain into Vmoto Soco. It is expected by the end of this year, it should have phased out and permanently closed its manufacturing facilities.

This agreement means that Vmoto retains exclusive sales and marketing rights for Vmoto’s own brand, E-Max, and Super Soco products globally, excluding China. To put it simply, Vmoto Soco would be focusing on international sales, further shifting its focus away from China. In my mind, this is a solid strategic move as competition and margin squeezing in China would make it hard for Vmoto to be as successful as I believe it can be in Europe and other international markets.

In addition, Soco Shanghai and Vmoto’s subsidiary Nanjing Vmoto reached a joint investment agreement to establish a new jointly owned company, Nanjing Vmoto Soco Intelligent Technology Co, Ltd. From this, Soco Shanghai retains exclusive sales and marketing rights for “Super Soco” products and is granted exclusive sales and marketing rights for “E-Max” products for the China market.”

As part of the agreements, “Vmoto Soco has the rights to use all brands, patents and moulds of Soco Shanghai for the manufacturing of the products, at no additional cost.” In a recent release, Vmoto stated that they had been forced to take certain legal actions to ensure Soco Shanghai met its obligations under the agreement. Whilst they believe this not to be material to the company, it does make you wonder whether conflicts will arise in future. For me, the business structure deserves half-marks. The China sales almost seem like a distraction from the core sales.

At the recent Milan EICMA motorcycle conference, Graziano Milano, the President of Strategy & Business Development of Vmoto Soco International, showed a slide of the rebranded Vmoto Soco Group. More on this below…

Vmoto Soco — The Rebrand & New Models

Vmoto Soco is in the process of rebranding. They recently changed their logo, and it certainly looks electric. I believe the brand needs to look ‘futuristic whilst still minimalistic’ to succeed. Retro looks will not compete with Vespa’s brand, so I’m happy to see this.

With this rebrand, Vmoto Soco presented three new models — The VS3, which comes under Vmoto Fleet, the Concept F01 and the Stash, which comes under the new Vmoto Premium brand. There hasn’t been significant detail released yet, but here is what I’ve found based on the Milan EICMA motorcycle conference that Vmoto Soco recently presented at.

The VS3 is a 3-wheel motorcycle designed for heavier delivery loads with a max speed of 45km/h, 450kg max-load weighting, and 250km of total range. If we consider the assumptions with prior models, I will assume this is also based on a 75kg person. The load weighting of 450kg is a big improvement on the VS2 (2-wheeler) E-max 160kg max-load weighting.

As part of the rebrand, the design of the Concept F01 looks much more modern and slick. Although the design is a big upgrade, the performance doesn’t appear much better than previous models. In the presentation, Graziano Milano says this is just L1, and L3 (a later version) will come a little later with “a higher speed just for light delivery where you may need a bike that has more power, faster, 6 hours of recharge in normal charge and 105kg of weight”.

He later goes on to say:

“So there is research. I can’t tell you much about it, but we are really accelerating the development of new technology to speed up the charging of our vehicles”

As to how long this may take? I have no clue, but it shows that performance improvements are a top priority, not just aesthetics.

We also got a look at the Vmoto Stash.

Yes, that is an electric motorbike…. Look’s like something out of Tron Legacy.

I’m a big fan of the Stash design. Performance-wise, it comes with 105km/h max speed, 250km range and 6 hours charging time. Like the Vmoto Fleet presentation, Graziano mentions the Stash will have a brother and sister with improved performance. These are all promising signs of what’s to come.

Are Management Competent, Capable & Aligned?

With managing director Charles Chen at the helm, I believe investors are in good hands. Charles boasts over 28 years of experience in motorcycle manufacturing and owns a little over 8% of the business, and is paid a salary of $350k p.a.

The rest of the board’s salaries are reasonable, and they collectively own ~1.85% of the business. Although this isn’t a great deal of skin in the game, when we look closer at the remuneration report, we can see that when comparing 2019 to 2020, the proportion of remuneration linked to share-based payments has increased from 22% to 58%. Hence, the board can’t just sit back & relax and collect an exuberant amount of salaries without growing the business.

It also looks like there’s been a push to increase the proportion of remuneration from share-based payments and performance-related payments for the other executives as well.

Whilst I’m content with the salary side of remuneration, I become a little less comfortable when we dig a little deeper into the performance and service rights. Maybe I’m being unreasonable, but I think the targets set here don’t seem challenging enough, nor do they seem to be long-term focused enough in my books. Taking this CAGR approach to offer even greater long-term incentives, I’d prefer to see these performance rights start vesting after 3–4 years.

For example, a three year period whereby they don’t vest fully for another 12–18 months after the three years.

Perhaps I’m too harsh, but I think this style of incentive promotes a greater focus on long-term CAGRs and incentivises long-term share price appreciation as well as ensuring management stay around to execute the long-term plans as all rights aren’t released from escrow until 1–2 years after the 3 year period.

Overall, I’m giving half-marks for this. Whilst it appears there has been a focus to increase incentives and remuneration linked to share price appreciation, I do feel it could have been done better. Although, I admit this is an area I’m still newer to so perhaps there was good reason for Vmoto to structure it in the way they have.

Thoughts about Financials

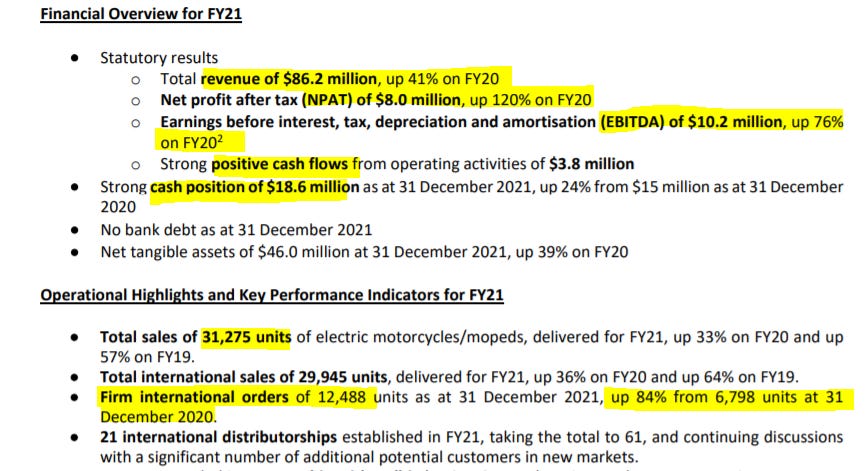

Vmoto recently released its full-year FY21 results. This included total unit sales of 31,275 for FY21, a 33% increase on FY20 and up 57% on FY19. The most important segment to my thesis, the international sales, was up 36% on FY20 and up 64% on FY19. This is reassuring with the focus being on international sales.

With no bank debt and $18.6m cash as of 31 December 2021, the company looks well-positioned for future growth. A leading indicator of growth being international orders was 12,488 units.

Normally, I’d be looking to see sequential growth, especially after the premium brand starts gaining traction. However, given unit sales can be lumpy (e.g. from a large order such as the Greenmo Group order) and sales can be seasonal, this may be misleading so we may not be able to infer a decline in the order book growth rate until at least a few quarters. Nonetheless, the international sales for FY21 were record sales, and we’re yet to see the impact of the rebranded Vmoto Soco.

The company is profitable and cash-flow positive, with full-year net profit after tax of $8m, a substantial increase from FY20 NPAT of $3.7m.

This is encouraging for the investment thesis. Top-line growth ->Margin expansion ->& NPAT growth growing at a faster pace.

Finally, if all these three hold true into the future, then we’d expect for the multiple that the market is willing to pay for Vmoto’s future earnings to expand too.

Clearly, we can see operating leverage kicking in. However, the question pertains as to how sustainable this is. In my opinion, until we see this sustainability Mr Market will not reward investors with a re-rate.

As a result, I’ll be keeping a keen eye on the growth filtering down to the bottom line. I’m hoping the premium brand allows for further margin expansion as well. Ideally, I’d want to see gross profit margins consistently above 25% and move closer to 30% over time.

Vmoto states that their manufacturing facility has the potential to scale up 10x of current production, around 300,000 units p.a. So, there is a large capacity for scaling up if new & larger orders come through.

Turning to the balance sheet, one thing that is interesting is that ‘trade and other payables’ shot up over 100% YOY. This forms part of the current liabilities and hence, I’m assuming this may be due to large purchases of parts from suppliers that are needed as the inputs for the electric mopeds/motorcycles. Perhaps this was in anticipation of the launch of Vmoto premium. However, it may also partially be a result of higher input prices due to global supply chain issues so it could be worth keeping an eye on. That being said, Vmoto is well-positioned with more than enough working capital at its disposal.

I believe the next 12–18 months will be telling. The market will have another year’s worth of ‘data’ to see how sustainable margins are, whether the margins can sustainably expand, and greater visibility on the potential of Vmoto’s premium brand.

At an NPAT of $8m, this places the P/E at ~13. This seems undemanding for a company that has grown revenue over 40% YOY and NPAT over 100% YOY. As a result, I don’t think it’s unrealistic to see Vmoto demanding a multiple closer to 25 (or at least 20) over the next 3–4 years, especially if NPAT doubles again in that time. Further, the EV/EBITDA multiple sits at ~10. A company growing as fast as this could be rewarded with a multiple closer to 15. However, we also can’t be sure this will happen. With the fear of rising interest rates, it’s perfectly possible the multiples people are willing to pay may contract. But, even if we assumed the multiple people were willing to pay remained relatively steady, I believe there is sufficient downside protection.

Of course, this may not eventuate as there are many moving parts to the business which could cause weaker than expected performance.

What could go wrong?

Given the current macroeconomic environment, the first issue that comes to mind is supply chain issues. The cost of shipping containers has risen dramatically, and so too has many inputs into the production of electric motorcycles. I envisage supply chain issues to dissipate over time. However, I am not sure how long this may take. I’ll certainly be watching for changes to margins and management commentary around this.

Secondly, whilst Vmoto can scale production up to 10x current capacity, saying this and doing this are two different things. Scaling up requires execution and can cause some headaches along the way. I am also not 100% sure how much more headcount this may require.

A big part of my thesis rests on Vmoto premium. If the new models here are not as well-received as I believe they should be, this could be concerning as I’m hoping these will provide an opportunity for margin expansion.

There will also be further competition going forward in this space. Monitoring existing competitors and new entrants will be necessary. More specifically, I want Vmoto to invest heavily in R&D going forward to improve the performance of future models, even if this impacts profitability in the short term. I do not doubt that Large ICE motorcycle companies will transition into the electric scene over time, just as we have seen in the car market. These companies have much more resources at their disposal, so this remains a considerable risk. If I don’t see the performance of new models improving over time (speed, charge time and range), I would probably consider the thesis broken as a moat cannot widen, even if their prices remained competitive.

The other significant risk involves execution in global expansion. New markets can have different jurisdictions, different market dynamics, cultures, demographics and so forth. The strategy to win new markets will need to differ, so management must identify the correct approach. These nuances could create challenges in the future.

What I’ll be watching in future

Order Book — Does there appear to be deceleration?

Repeat customer orders — Do they keep coming back, and are the order sizes increasing or decreasing?

New B2B wins

Where they choose to expand to — I personally feel Australia is not ready for Vmoto yet, and so I hope Europe remains the major focus for some time.

Vmoto Premium — How much does this positively or negatively impact sales and profitability. I’d like to get a better sense of demand here.

Style of business for global expansion — e.g. expanding into India — how do they make this work, given localisation laws.

Overall, Vmoto looks to be ticking along very nicely. From an investment perspective, there are more moving parts than I’d normally be comfortable with. However, I can’t argue with management’s execution so far. There appears to be multiple shots at goal — Repeat orders, new B2B customer wins, potential expansion into India and the new premium range. I’m excited to see how Vmoto can capture International markets and I think secular tailwinds present a fantastic opportunity in 2022 and beyond. At this stage, I’m not sure this will become a major position for me(on a cost basis), purely because of the nature of the industry. However, I do hope this company does well as we move towards a greener world so I’ll be following the story closely.

On a final note, some food for thought…

The trend towards reducing vehicle carbon emissions is becoming increasingly known, socially expected, and required by policy and law in many countries. There’s no doubt that EVs are the way of the future, but the trouble is figuring out which ones are best placed to take advantage of the megatrend.

Is it the incumbents? Is it the new entrants? Or is it a company we are yet to see?

For example, in hindsight, it’s easy to say now that you should have invested in Tesla over a decade ago. But ten years ago Tesla was arguably too early to the trend and moved sideways for many years before it finally sky-rocketed to where it is today. Being a holder over all those years of relatively flat movements required a high degree of conviction & patience.

If we look further back to the late 1990s, the dot-com bubble saw internet-related companies sky-rocket before busting a few years later in the early 2000s causing companies to plummet and many others to go bust altogether. The point is, whilst the trend might be clear, understanding which companies can become the ‘Gorillas’ is far more difficult and will distinguish investors from speculators. Having the conviction to hold throughout years of minimal share price movement or even large run-ups and subsequent draw-downs will determine how well one does over the long term.

Most of the “Gorillas”, have had sustained periods at some point of little to no share price movement and even large draw-downs before reaching new highs. Investors without conviction can sell too early in these cases, therefore missing out on most of the upside. This is why understanding the company’s fundamentals, and your thesis is crucial for navigating these megatrends as volatility will be high.

I expect high volatility, and I am comfortable with that for the most part. Still, I also know that on a psychological level, I am more likely to take profits too early on winners if I haven’t done the work and don’t carry enough conviction. I’m trying to remind myself that winners tend to keep winning even if valuations get stretched at times in the short term. The point is, if you are getting caught up in the ‘hype’ and the ‘megatrends’, try to place some extra focus on understanding these companies inside and out, perhaps even more than portfolio ‘staples’.

I hope readers enjoyed this write-up.

As always, please read the disclaimer below.

Disclosure: At the time of publishing, I own shares in Vmoto (ASX:VMT) and LaserBond (ASX:LBL).

Disclaimer:

The contents of this article, including the links provided, are general in nature and DO NOT consider your personal situation, risk appetite, goals, and objectives. The information contained in this article is for education purposes only and should not be construed as professional advice, nor should it be substituted for an independent financial adviser. The author is not a licenced financial professional. They are expressing their own views, opinions and experiences, which does not take into account the specific situation or needs of readers. As such, all readers should consult an independent licenced ASIC financial professional before making any financial decisions concerning the contents of this article. The author will not be responsible or liable, directly or indirectly, in any way for any loss or damage of any kind incurred as a result of, or in connection with, your use of, or reliance on, any of the contents of this article. The author may own particular financial products mentioned in the article. Nothing in this article is considered a buy, hold or sell recommendation regarding any company, nor is it a recommendation to buy or sell any financial product or service mentioned in the article. Finally, remember, the author’s opinions and views are subject to change over time with new and/or different information.

By viewing the contents of this article, you agree: (1) you have read and understood the warning and disclaimer above; (2) not to make any decision based on the contents of the article; (3) not to place any reliance on the contents of the article; and (4) that the author is not responsible or liable, directly or indirectly, in any way for any loss or damage of any kind incurred as a result of, or in connection with, your use of, or reliance on, any of the contents of this article.

Thanks for the write-up. I really enjoyed your thoughts on the perfomance rights plan!!! I bought some last Friday. I too am a little uncomfortable with the way the performance rights are organised. I think the ceo is a bit overpaid but perhaps that's cause I'm bad at calculating australian dollars. He recently bought some more. I am a bit concerned about the friendlyness to shareholders with this company. The indian deal fell in the water. In Europe they are mostly seen for the fooddelivery services, I haven't really seen them elsewhere, which explains the low bag lock. The real sales will be from Asian countries I think in the future. They seem to be one of the cheaper models on the market. The stash design like tron legacy does look good. They're working together with Ducati and an Italian investor now who was granted an option on 10% of the company. I don't really undersstand how this company after 10 years of doing nothing has a net cash position, they must have really screwed investors when they IPO'd. Their cash flow is going in the right direction but has been a bit low imo.